Using Regulatory Capital to Maximise Yield with Digital Assets

With the help of technology, financial institutions can now leverage shariah-compliant sukuk products as high-quality liquid assets ("HQLA") while meeting regulatory capital requirements.

“From Burden to Opportunity: Using Regulatory Capital to Maximise Yield with Digital Assets”

With the help of technology, financial institutions can now leverage shariah-compliant sukuk products as high-quality liquid assets ("HQLA") while meeting regulatory capital requirements.

High-quality liquid assets (HQLA) are crucial to ensuring the stability and resilience of the global financial system, providing a buffer against potential liquidity shocks. These assets help to mitigate systemic risks by ensuring there is sufficient capital to support ongoing business operations in times of market turmoil, and to protect a financial institution's clients from potential losses.

Not surprisingly, HQLA are a key component of the capital requirements imposed by regulatory authorities - which state that institutions must hold a certain amount of assets that meet specific criteria, such as being highly liquid and having a low correlation with risky assets. Examples include government bonds, certain corporate bonds, and cash held with banks.

Requirements vary by jurisdiction, but most global banks follow market-leading standards set by the Basel frameworks - under which the assets of banks are risk-weighted to ensure safer investments, with government bonds having lower weights than corporate loans. Riskier assets require more high-quality tier 1 capital - mainly common equity and retained earnings - to absorb potential losses. Banks must hold tier 1 capital equivalent to at least 6% of their risk-weighted assets, which is calculated by taking each asset's value multiplied by its risk weight.

Government bonds are typically considered low risk and highly liquid, but can often be difficult to access, and may not produce the best yields - especially after distribution costs. Corporate bonds, on the other hand, may offer higher yields but come with a certain level of credit risk, and are likely to be considered level 2 (L2)HQLA.

Choosing the right asset

The obvious choice for low-risk, higher-yield deposits would be US Treasury bills - but these come with a number of disadvantages, especially given recent downturns in the bond market - they are also not an option for Islamic institutions, as such instruments pay interest or ‘riba’ - a concept disallowed in Islamic finance.

One common default approach to accessing HQLA is to hold fixed deposits, which provide a stable source of liquidity. While this ensures compliance with regulatory standards, it often results in lower yields and limited flexibility in managing assets.

While meeting the criteria of HQLA with low-yielding deposits may be seen as a burden or a mere cost of doing business, there are still untapped opportunities to transform these “regulatory” requirements into a source of improved yields.

Through the combination of a high-yielding asset, such as a quality sovereign bond issuance, the efficiency of digitalisation, and standardised legal and custodial arrangements, unique opportunities to access higher yield can be unlocked.

CASE STUDY - TOKENISED SUKUK AS REGULATORY CAPITAL

Financial institutions operating in the Labuan International Business and Financial Centre (Labuan IBFC) enjoy benefits typical of offshore jurisdictions, such as an efficient regulatory framework and competitive policies. Yet they still need to meet regulatory capital requirements - which, depending on the type of licence (banking, insurance, trust, captive, etc) - includes paid-up capital, a surplus of assets over liabilities, and risk-weighted capital ratio requirements.

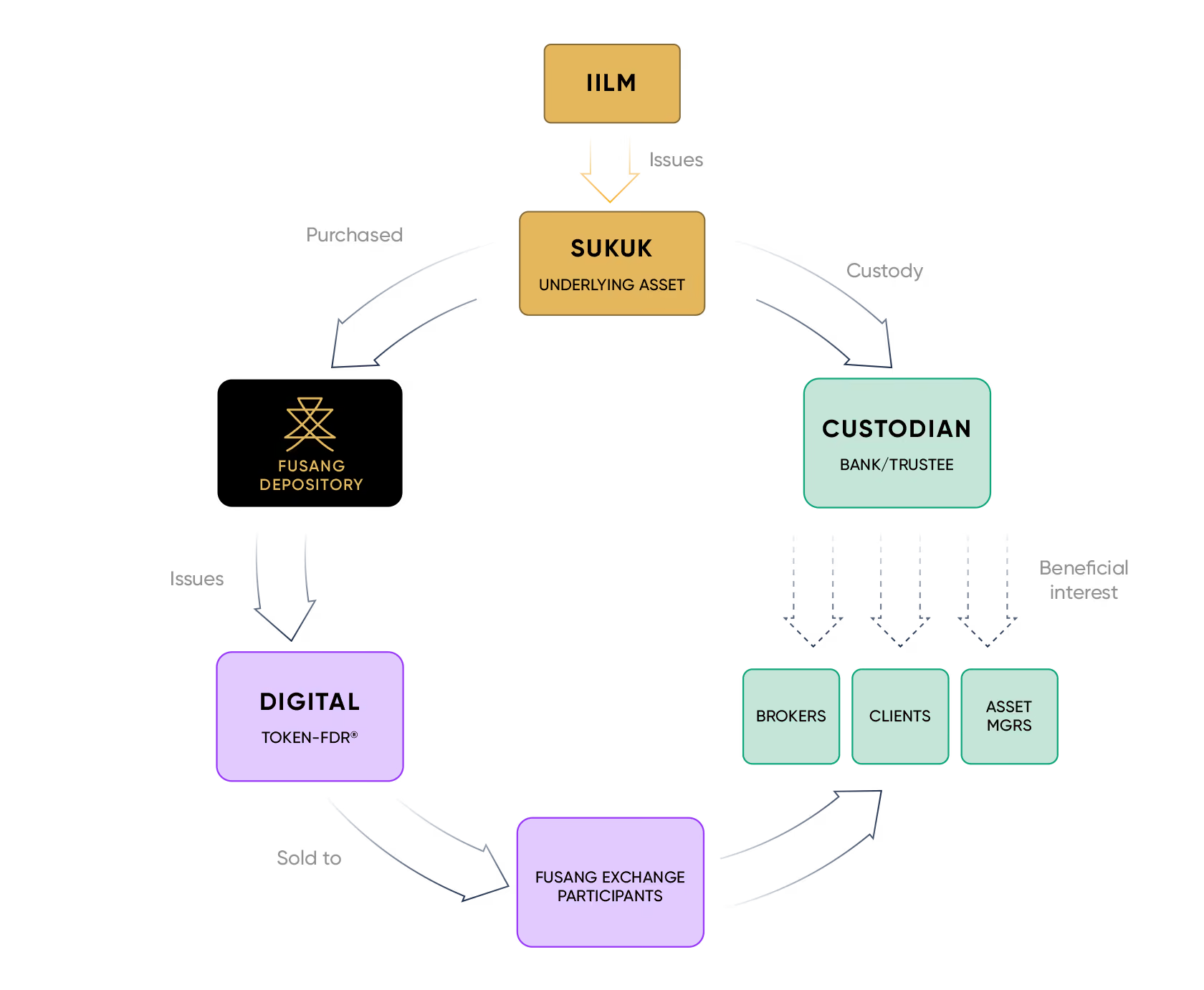

In order to create more liquid shariah-compliant financial instruments, the International Islamic Liquidity Management Corporation (IILM)*, an international organisation established by eight central banks and one multilateral organisation, regularly issues short-term sukuks in USD, helping facilitate cross-border Islamic investments while maintaining financial stability.

Fusang has developed an innovative tokenised sukuk, which has recently been issued as a shariah-compliant option to financial institutions and regulated entities in Labuan IBFC, Malaysia. This tokenisation exercise is the world’s first digitisation of an institutionally-issued sukuk, and is expected to revolutionise the Islamic investment landscape by providing investors access to shariah-compliant high-quality liquid assets (HQLA).

The tokenisation and listing exercise was completely led by Fusang, utilising its proprietary Fusang Depository Receipt (“FDR”) structure to “wrap” the underlying sukuk into digital form. The FDR retains full transparency and certainty of investors' legal rights, and adheres to Shariah standards set by the Accounting and Auditing Organization for Islamic Financial Institutions (“AAOIFI”). ZICO Shariah Advisory Services acted as the Shariah advisor for the issuance of these ERC-20 compliant tokens - the leading and most popular Ethereum standard for token issuance.

Similar to American Depository Receipts (“ADRs”) and Hong Kong Depository Receipts (“HDRs”), FDRs represent a beneficial interest in an underlying security, which can then be listed, traded, and settled on the Fusang Exchange. FDRs are fully redeemable for the underlying IILM sukuk, and are secured by third-party independent custodians. FDRs ensure all parties have uniform legal rights and custodial arrangements.

The resulting tokenised sukuk is sanctioned as sharia-compliant by one of the largest Shariah advisory firms in Malaysia. These sukuk offer investors a profit rate that mirrors or exceeds returns from US Treasury bills, creating an efficient sharia-compliant liquidity management tool for Islamic financial institutions, much as conventional financial institutions use short-term government-backed bonds. This tokenised sukuk has already been deployed by Fusang and is being used to meet the regulatory capital requirements of our own group of companies, making it a tried-and-tested method which can also be used to help other financial institutions maximise returns on their own regulatory capital with minimum friction.

This new option offers Labuan-regulated entities a competitive edge, while adhering to Islamic finance principles. The tokenised sukuk also offers a shariah-compliant alternative to traditional HQLA assets, providing a way for institutions in Labuan and globally to adhere to their prudential regulatory requirements, based on ethical principles - thus turning regulatory and ethical compliance into an opportunity for growth and innovation.

*Disclaimer: This article is not intended to indicate participation, expressly or implicitly, on the part of IILM or any of its shareholders in this tokenisation exercise.

For more information, see this info sheet:

www.fusang.co/news/tokenised-sukuk-info-sheet

Enhancing yield on Regulatory Capital

Thanks to market innovations, financial institutions can explore opportunities to improve their capital efficiency by seeking quality issuances and returns simultaneously. By carefully selecting their HQLA portfolio, institutions can enjoy gains while maintaining compliance with regulatory requirements. This involves a thorough analysis of available assets, considering factors such as credit risk, liquidity, and potential returns. By adopting these innovative strategies, institutions can further enhance their yield potential.

Don’t miss out on the latest opportunities. For more information about Fusang Exchange and our tokenised offerings, get in touch with us today at [email protected]